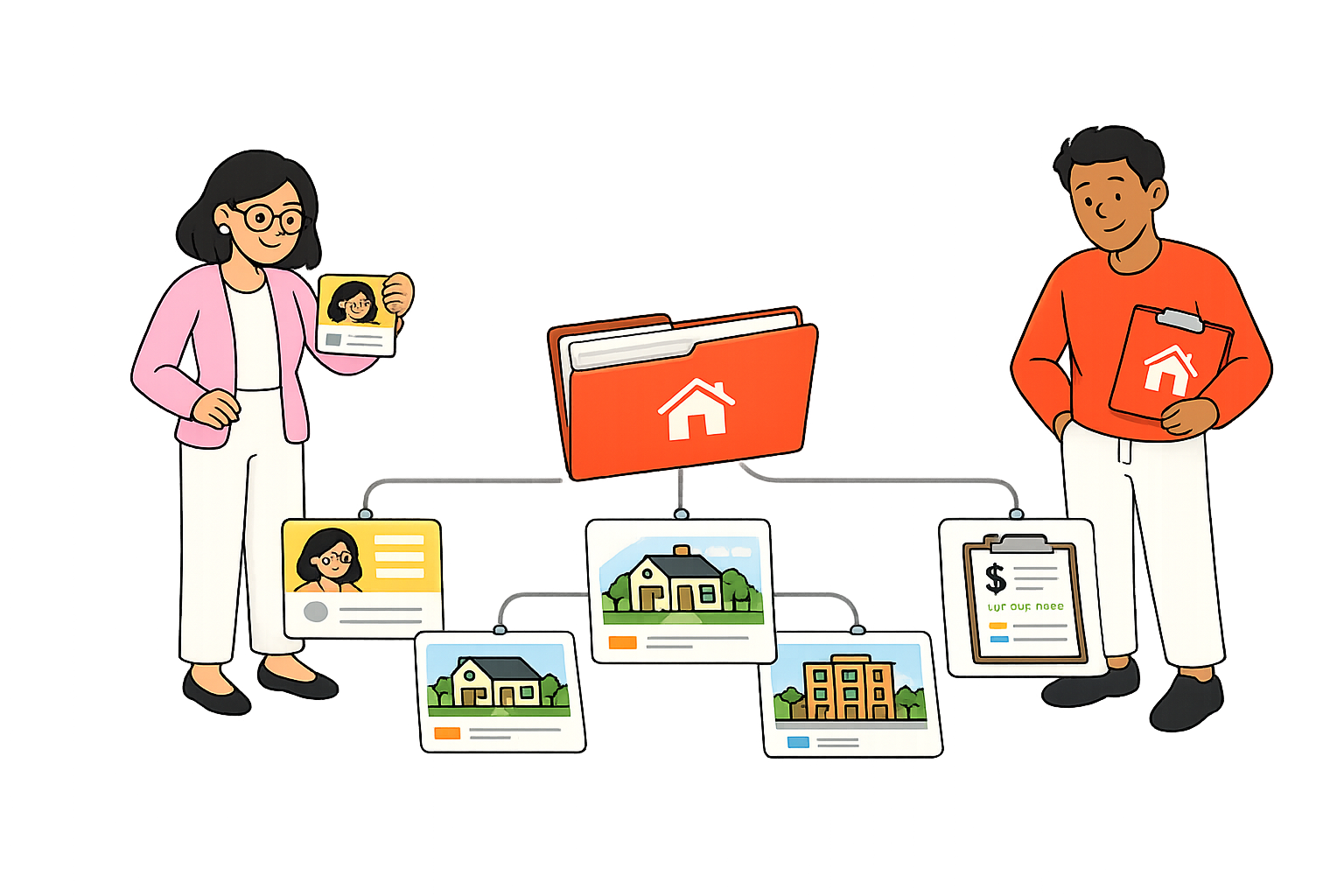

Portfolio shell

The top-level portfolio sets the container that the rest of the app reads from.

Portfolio setup, property tax, suburb research, cashflow, retirement, and scenarios all read from one set of records.

The point of the product is not to hide complexity behind one number. It is to keep the source facts, current ledgers, and decision outputs close enough together that you can still inspect the working.

The base records are what make the later decision pages trustworthy.

The top-level portfolio sets the container that the rest of the app reads from.

Income, assets, debt burden, and tax settings sit at the person level so ownership and affordability stay grounded.

Household spend stays alongside rent, wages, debt service, and retirement capacity.

Linked loans drive repayment, interest, refinance analysis, debt service, and current cashflow.

Each property keeps rent, costs, value, improvements, title allocation, and local market context together.

Current cashflow, tax, debt, and market context come first so future assumptions have a real starting point.

Cashflow pages start with the current household result before any future-year assumption is touched.

Annual tax result, owner-level split, claim support, and sale treatment stay beside the same property facts.

Portfolio health targets and suburb benchmarks show whether the current mix matches the direction you want.

Annual ledgers, cash-versus-tax bridges, and tracked capital improvements keep the result explainable.

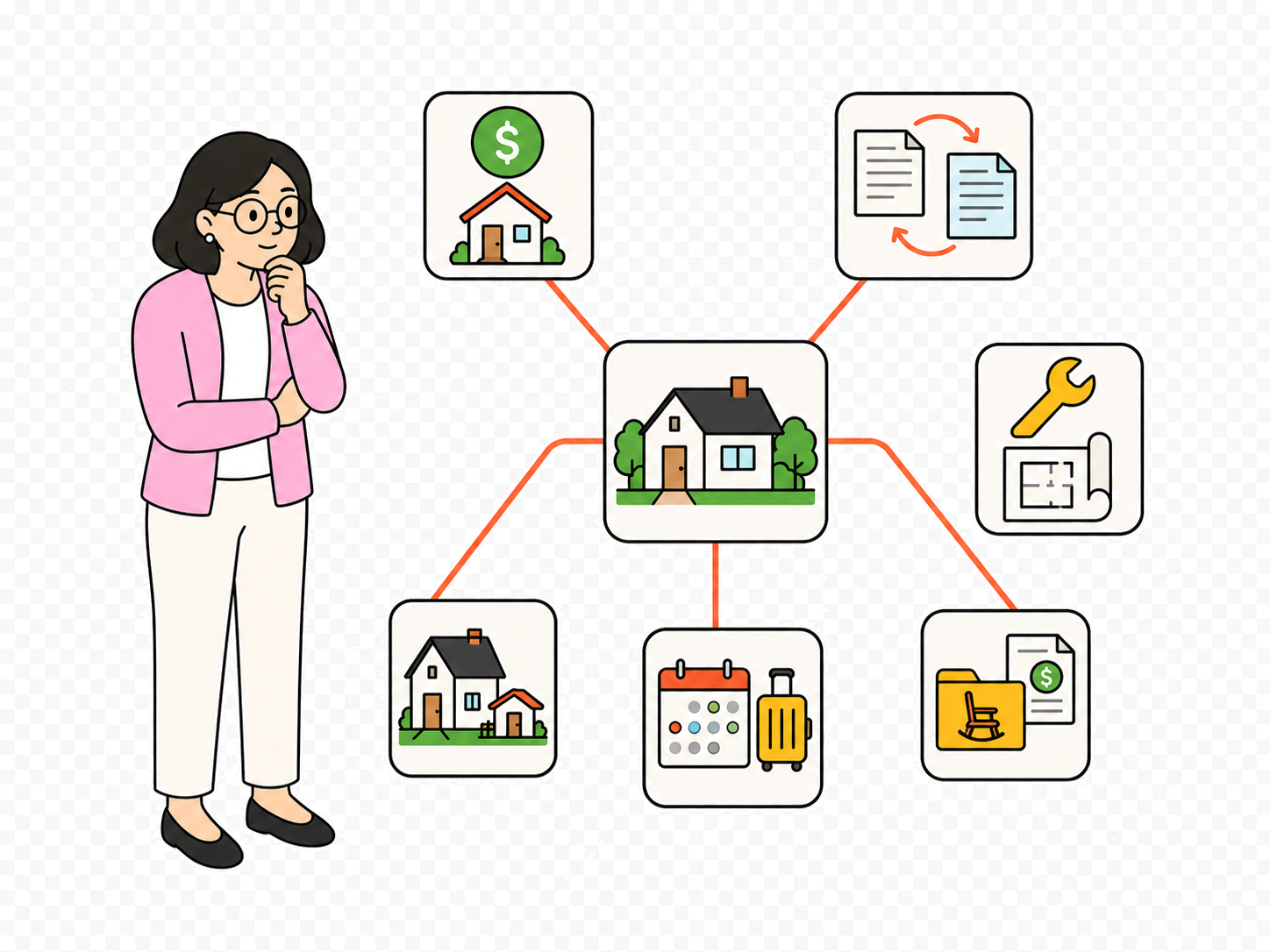

The scenario and retirement views are designed around the decisions people actually need to make.

Compare sale proceeds and reinvestment against continuing to hold the selected property.

Replace the linked loan and inspect the payment change, costs, and long-run outcome.

Test project cost, funding structure, tax treatment, and payoff horizon on the selected property only.

Compare long-term rent against short-stay use after occupancy risk, setup costs, and fee drag.

Read whether the current portfolio supports retirement and what sale cash is left after debt, costs, and tax.

Move from the product structure into the actual property choices: sell, refinance, renovate, short stay, granny flat, and retirement.